Rare Earth Reshoring: how Falcon can free up capital and improve supply chain security

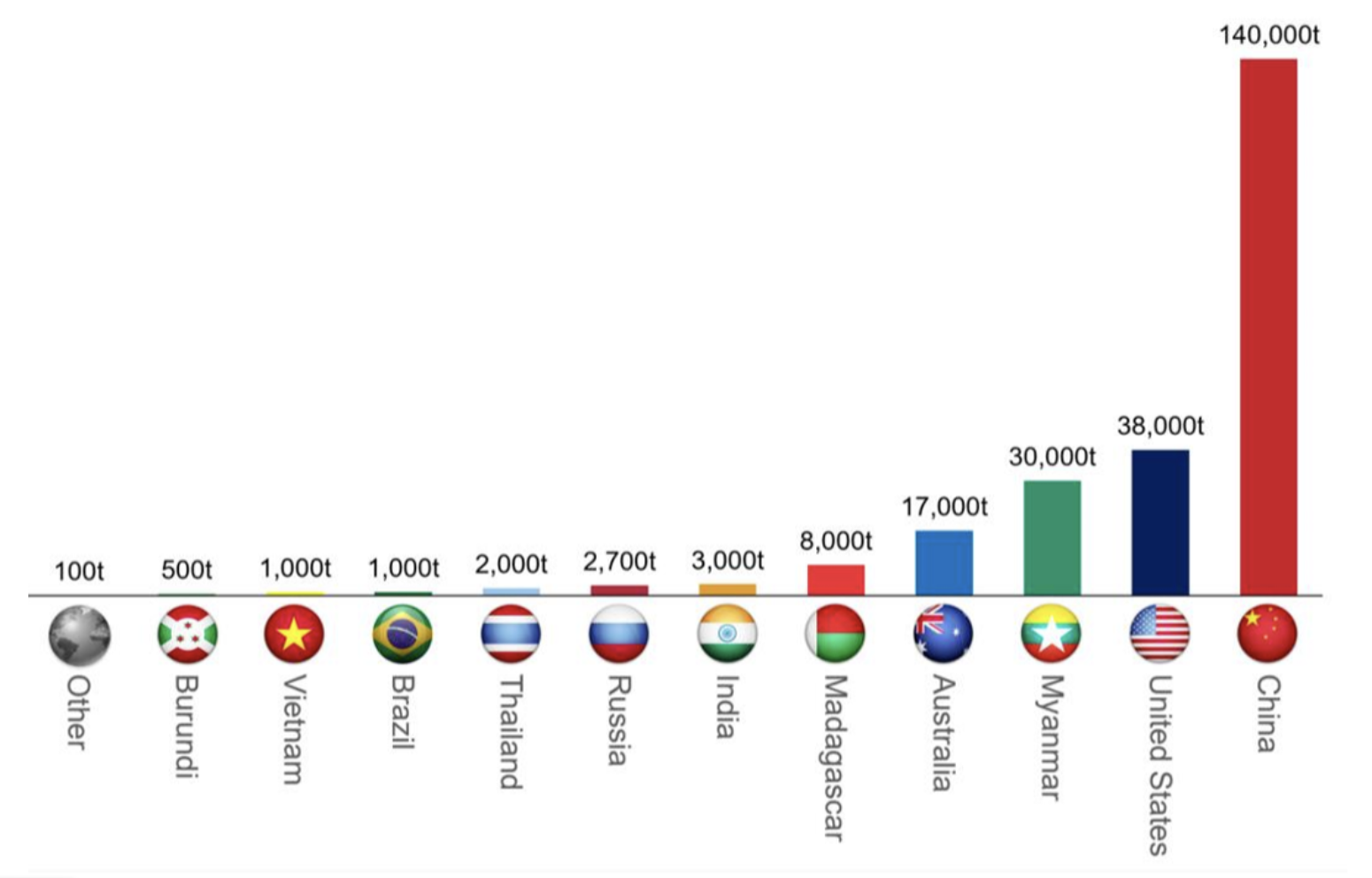

China controls the vast majority of the world’s supply of rare earth metals and minerals. This matters.

Rare earth metals play a critical role in defence technology and electric vehicles (EVs), as well as being crucial for motors, turbines, iPhones, and medical devices. Scarce minerals such as lithium, nickel, and cobalt are all critical to battery operation, performance, and longevity, and copper and aluminium are vital for any functioning electric network.

A recent merger of three Chinese rare earths mining companies (China Minmetals Rare Earth, Chinalco, and Ganzhou Rare Earth Group) will create a new super entity, dubbed an ‘aircraft carrier’ by state media, further cementing China’s dominance. News of the merger will only increase US determination to claw back some of China’s 85% market share. The California-based Mountain Pass mine is the focus of a renewed US strategy to fully reshore the rare earth supply chain. Elsewhere, the Lynas Corporation recently received $30m in Pentagon funding to build rare earth processing facilities in Texas. Washington is also looking to Mexico, Canada, and Greenland as a source of rare earths and scarce metals.

Unfortunately for Washington, China has already stolen a march on the US by investing heavily in rare earth mining operations in Asia, Africa, and Latin America. New mining activity is also heavily scrutinised for its ecological impact. Lynas has faced environmental protests in Malaysia, and Serbian authorities recently suspended plans for Rio Tinto to begin mining lithium amid fears over the impact on rivers and farmland.

To mitigate these concerns, some companies have proposed extracting rare earths from coal, and the recycling of raw materials used for EVs is receiving greater investment focus. However, the jury is out on the practicality and cost efficiency of such initiatives.

Rare Earth Metals and Scarce Metals Production by Country, 2020

Despite these challenges, America’s determination to close the rare earths gap with China should not be underestimated, with the Biden Administration’s trillion-dollar Infrastructure Law focusing heavily on strengthening supply chains. There may also be a long-term focus on finding a substitute for rare earths or even retooling products so that they are no longer required. BMW and Tesla have started producing EV batteries that do not require rare earth metals, and the world’s two largest carmakers, Toyota and Volkswagen, are striving to reduce their reliance on rare earths.

That said, developing alternatives to rare earths will clearly be expensive, and reshoring and ramping up domestic US extraction and production will take time. From an inventory management perspective, while the lengthy process of shortening rare metal supply chains plays out, there will be a continued focus on storing associated buffer stock on a Just in Case (JIC) basis. The reality is that supply chain disruption has been unrelenting in recent years, and companies are understandably skittish about following the Just In Time (JIT) inventory model pioneered by Toyota in the 1960s. Despite the downsides of trapped capital, JIT’s less glamorous but more reliable JIC counterpart looks like the safer bet. The semiconductor shortage cost the automotive industry an estimated $210 billion in revenue in 2021. A repeat of this just isn’t an option.

Is there a viable alternative? Does the choice between JIC and JIT have to be so binary? Falcon Group offers a third way. In its simplest form, Falcon’s model means it owns your inventory and makes it available when you need it. In the meantime, inventory is held in your own warehouse or in a geographically relevant third-party facility, with Falcon holding inventory on its books until required. This liberates trapped capital but also fosters more agile supply chains, facilitating near-shoring and reducing the need for emissions-heavy emergency air freight. In more complex models, Falcon’s agility and expertise mean it can insert itself effectively between a customer and multiple suppliers, ensuring the smooth and timely flow of goods and funds throughout the supply chain.

Reducing rare earths dependence on China and reshoring production will take time. Supply chain disruption will continue and even intensify, and manufacturers need to be ever more resilient. Fortunately, asset-light balance sheets and unlocked capital do not have to be sacrificed at the expense of supply chain security. Falcon’s third way offers the best of both worlds.