From Shortages to Strategy: How Semiconductor Leaders Can Build Resilient Supply Chains

Understanding the Cyclicality of the Semiconductor Industry

The semiconductor industry is inherently cyclical, characterised by alternating phases of growth and contraction driven by a confluence of supply and demand factors. This oscillating nature, with each cycle bearing unique characteristics, is fundamental to the sector. A significant boom in 2021-2022, followed by a slight correction beginning in late 2022, exemplifies this pattern. During the boom, soaring demand created a severe chip shortage, disrupting multiple sectors. The 2021 deficit stemmed from a complex interplay of factors, primarily the COVID-19 pandemic and the resulting supply chain squeeze, along with its impact on consumer behaviour.

This combination of factors led to a prolonged global semiconductor shortage, affecting various industries and causing significant disruptions in production and supply chains. The implications were severe, with many companies experiencing inventory stockouts and substantial revenue losses due to the demand-supply imbalance. For instance, Jaguar Land Rover’s retail sales fell by 37.6% compared to the same quarter in the previous year, primarily due to the chip shortage (BBC, 2022).

Inventory Trends and Financial Implications

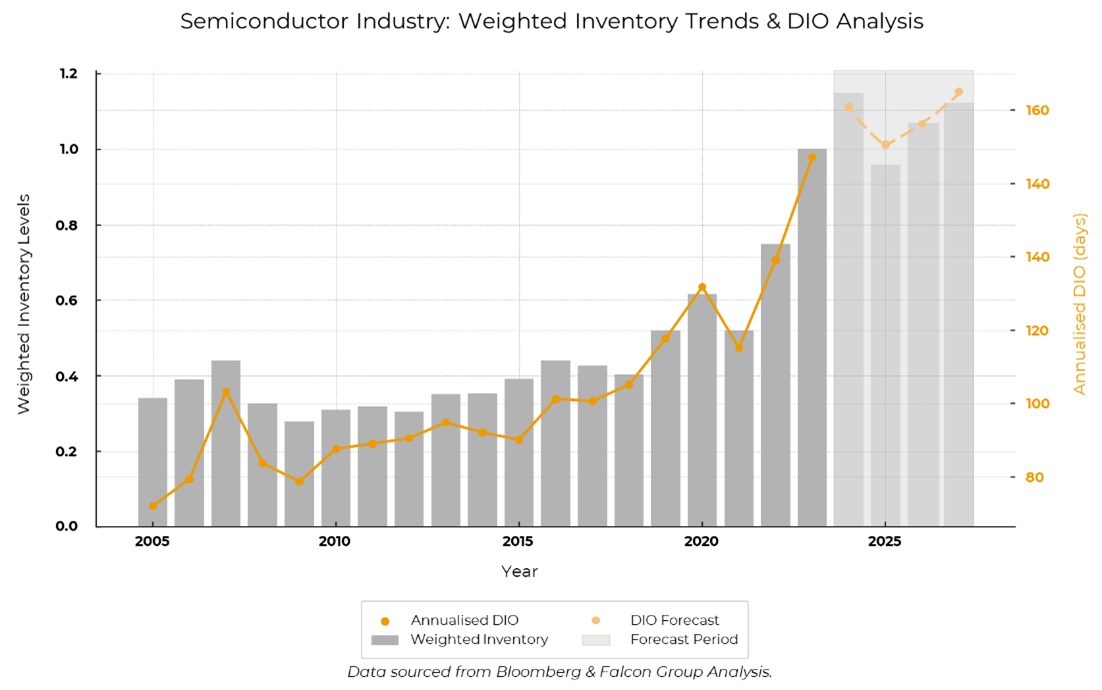

The semiconductor industry has experienced accelerated inventory buildup since 2020, as companies extend holding periods. This has come about as a strategic response to an amalgamation of supply chain disruptions, increased demand for semiconductor products, and changes in procurement and production policies. Figure 1 illustrates the upward trends of both inventory levels and the DIO across the sector. Elevated inventory levels could strain working capital unless supported by off-balance sheet financing or supplier credit.

The semiconductor industry has faced a prolonged period of supply chain uncertainty, driven by geopolitical tensions, raw material shortages, and fluctuating demand-supply dynamics, exacerbating production delays and cost volatility. While not at its peak, the industry is ticking towards recovery and expansion. Forecasts from WSTS and Bank of America predict strong semiconductor market growth in 2025. WSTS projects a 12.5% year-over-year increase, bringing the market to $627 billion (WSTS, 2024). Bank of America expects 15% growth, reaching $725 billion, driven by a 20% rise in memory sales and a 13% increase in core semiconductors (Bank of America, 2024).

Cost Structure and Cyclical Volatility

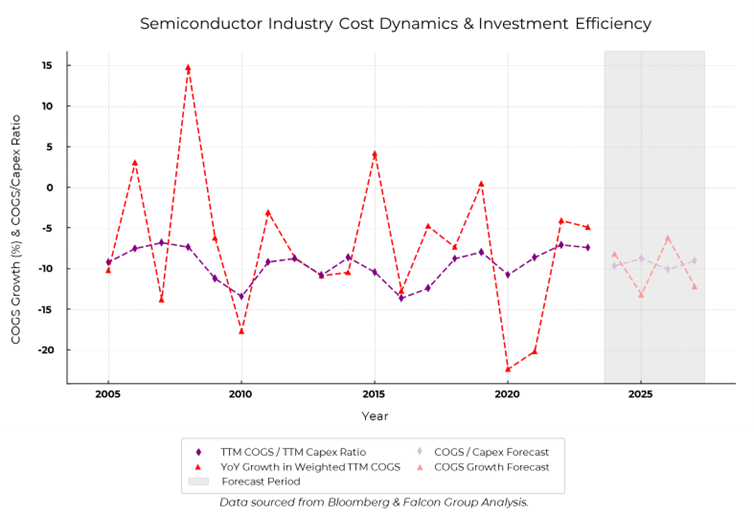

Figure 2 highlights the semiconductor industry’s volatile cost structure, with COGS growth (red dashed line) showing sharp spikes and contractions, reflecting fluctuations in input costs, supply chain disruptions, and demand shifts. The COGS/Capex ratio (purple dashed line) remains largely negative, indicating frequent periods where cost growth outpaced investment. Notable stabilization between 2010–2015 suggests improved capital efficiency, but overall, the industry’s cyclical nature forces companies to continually adjust spending. Persistent swings in COGS growth underscore the challenge of balancing cost efficiency with capacity expansion amid geopolitical and supply chain pressures. This volatility is further compounded by ongoing disruptions in global supply chains, where geopolitical tensions and raw material shortages have intensified cost fluctuations and procurement challenges.

Navigating Lead Time Extension and Price Instability

Lead-time extension and price instability in the semiconductor industry have become critical focal points in recent discussions, particularly as supply chain disruptions persist and demand for chips remains elevated across sectors like automotive, AI, and consumer electronics. Extended lead times, often exceeding 20-24 weeks for key components, exacerbate inventory financing challenges, as companies must allocate more working capital to maintain safety stocks, thereby straining liquidity. Concurrently, price instability, driven by fluctuating raw material costs (e.g., rare earth metals) and geopolitical tensions (e.g., U.S.-China trade restrictions), creates uncertainty in forecasting and budgeting, impacting profitability. Additionally, tariffs on critical semiconductor components and equipment have further strained global supply networks, increasing costs and complicating procurement strategies for manufacturers. These factors are likely to persist into 2025, urging firms to adopt more agile inventory strategies and hedge against price volatility by taking measures to enhance supplier resiliency.

Building a Resilient Supply Chain

Ensuring adequate inventory is crucial, but this must align with balance sheet considerations. Buffering strategies help mitigate risks but must be carefully managed to avoid excessive capital tie-up that could otherwise support growth and innovation.

Given the industry’s dynamics , firms must proactively manage inventory and working capital to stay competitive. Given these challenges, firms must explore alternative financing and inventory strategies to remain agile. One approach is third-party inventory ownership, which can provide financial flexibility and supply chain resilience. This is where third-party inventory ownership becomes accretive. Falcon Group’s approach offers significant benefits:

- Financial Flexibility – Off-balance sheet solutions enable strategic inventory management without balance sheet burden.

- Working Capital Optimisation – Falcon frees up capital for innovation and growth by taking ownership of inventory and selling it to clients on a just-in-time basis.

- Cost Reduction – Bulk purchases and upfront settlement discounts can lower costs while improving efficiency.

- Supply Chain Resilience – Falcon aligns with a buffering strategy to manage disruptions.

- Improved Relationships – Can alleviate the burden that arises between suppliers and customers over inventory ownership.

- Operational Efficiency – As a single point of contact for multiple suppliers, Falcon can help streamline inventory management.

Falcon Group helps semiconductor companies manage cyclicality, improving resiliency while mitigating risks tied to long lead times, inventory, and supply chain disruptions.

References

- BBC News. (2022). Jaguar Land Rover (JLR) lost £3.5bn in 2022 despite strong sales. BBC News. Available at: https://www.bbc.co.uk/news/business-60211153

- World Semiconductor Trade Statistics (WSTS), 2024. Recent news release: Fall 2024 forecast. WSTS. Available at: https://www.wsts.org/76/Recent-News-Release

- Bank of America, 2024. Semiconductor Outlook for 2025: AI Boom and Shifting Market Dynamics. Available at: https://theoutpost.ai/news-story/bank-of-america-s-2025-semiconductor-outlook-ai-boom-and-shifting-market-dynamics-9618/